Understanding Perpetual Market Funding

At the heart of each perpetual market is the funding rate. The funding rate helps keep the price of a perpetual close to its index price by incentivizing traders to buy when the price is low relative to the index and to sell when the price is high relative to the index.

Without a well-designed funding rate, the price of the perpetual may deviate systematically from the index price, which may make the perpetual less efficient and riskier to trade, and may disincentivize liquidity providers.

While funding rates across exchanges tend to share the same major components, no two are the same. Differences in funding rate designs are likely to affect price dynamics in ways that are subtle but nevertheless significant.

Funding rates can also be used to generate crypto dollar yields by investors who take the receiving side of the funding payments. The yield offered by perpetual funding is often larger than that of most financial products available in traditional finance.

Funding rates play an important role in crypto markets today because of just how much global trade volume is concentrated in perpetual products. As we discussed in our recent article comparing perpetual exchanges, perpetual markets have found very strong demand among crypto traders because they offer a convenient way to hold leveraged positions without an expiry date. Unlike futures contracts, perpetuals don’t need to be regularly rolled over in order to maintain one’s exposure to a position.

The purpose of the funding rate is to encourage the price of a perpetual contract to trade close to the price of the underlying, both over the long term and the short term. A good funding rate makes it easier to predict and understand the price of the perpetual, which is important for attracting both traders and liquidity providers. Another way to frame the funding rate is as the cost to hold either a long or short position, similar to how margin exchanges charge interest on borrowed capital. A well-designed funding rate allows the price activity of the perpetual to almost exactly mirror the underlying spot market. The BitMEX BTC–USD contract provides a good example of this, and of the success of the funding rate model that they pioneered.

After BitMEX saw success with their perpetual contract, various crypto exchanges rushed to launch their own perpetual products. The main ideas from BitMEX’s original funding rate design remain unchanged in most perpetual markets, still, no two perpetual markets use exactly the same design. We’ll examine these differences in more detail below.

We will also discuss how perpetual market funding rates can be used as yield-generating instruments. Within a given perpetual market, any position collecting funding is subject to market risk. The key to using perpetual funding as a source of yield is to hedge that risk out of the equation.

How do funding rates work?

Funding rates work by putting a price on any deviations that occur in the perpetual market price relative to a target price which is either equal to or derived from the spot price of the underlying. When a perpetual consistently trades above its target, it is assumed that longs are more in-demand, and so traders holding long positions will make payments to traders with short positions. On the other hand, when a perpetual market consistently trades below its target, it is assumed that shorts are more in demand, and so shorts will pay longs. The greater the deviation between the perpetual price and the target price, the greater the magnitude of the funding rate.

When calculating funding payments, the funding rate is applied to the notional size of a trader’s position. This means that traders with higher leverage will pay more, relative to the collateral securing their position. Funding rates can be applied at various points in a position’s lifecycle, but most perpetual markets either charge funding once every eight hours, once every hour, or continuously.

Two important concepts in the funding rate calculation are the index price and the mark price. The index price is an average of spot prices from various exchanges and the mark price is derived from the index price, sometimes including a decaying basis rate that accounts for the amount of time until the next funding payment. The mark price is the primary reference price used throughout the calculation of the funding rate.

Within the funding rate calculation itself, there are typically two main components: an interest rate component and a premium component. The interest rate component is usually a constant, which may depend on the particular assets underlying the perpetual. In the case of the dYdX and BitMEX perpetual markets, the interest rate component is fixed at 0.01% per eight hours. Meanwhile, the premium component quantifies how far the perpetual market is trading from the mark price. It is often calculated as the distance between the mark price and the impact bid and ask prices, which are defined as the prices necessary to clear the bid and ask sides of the orderbook, respectively, by a predefined amount. The smaller the distance, the lesser the premium component. As an example, BitMEX uses the following formula:

Premium Index (P) = (Max(0, Impact Bid Price - Mark Price) - Max(0, Mark Price - Impact Ask Price)) / Spot Price + Fair Basis used in Mark Price

Most funding rate designs apply a time-weighted average when calculating the premium component. A time-weighted average is preferred as a sampling method in order to make manipulation of the funding rate more difficult. The exact timing of the sampling can be randomized as an additional precaution. The funding rate is then calculated by summing the interest rate component and the average premium component. The most popular perpetual markets will also apply a clamp function, which requires the premium to be of a certain magnitude before it will affect the funding rate. Other funding models do not use a clamp, for example, the funding rate calculation for the dYdX BTC–USDC perpetual market is simply the following:

Funding Rate = One-Hour Premium + Interest Rate Component

Funding Rate Design

Funding rates are not one-size-fits-all. All designs have tradeoffs and exchanges have a big incentive to find a funding rate that users will trade with the most. Given that BitMEX has been a pioneer and leader in perpetual markets in terms of volume and open interest for some time, most funding rates are based to some extent on BitMEX’s funding rate formula.

Binance

Binance largely used BitMEX’s design, but with a few changes. Binance doesn’t factor in a funding basis when calculating the premium component, which essentially means that funding rates don’t rely on or have memory of previous funding rates. Binance calculates its funding rate every second, which only relies on the premium component that second.

ByBit

ByBit also largely stuck with BitMex’s design, with one notable change. On ByBit, funding is calculated every eight hours, but that funding rate isn’t applied until the following funding period. It’s unclear exactly what this accomplishes.

FTX

FTX has one of the more unique funding rate designs in the space. Unlike most exchanges where the premium component is scaled so as to be realized over an eight-hour period, premiums on FTX are calculated every hour but scaled to have a realization period of 24 hours. This means that a price differential of a given size will result in relatively less funding. Similar to Binance, FTX doesn’t factor in a funding basis when calculating the premium component. Instead of using an impact price for the mark price, FTX uses a mark price which is simply the median of last bid and last ask, which could introduce more volatility into the funding rate, compared with other designs. Finally, FTX doesn’t use an interest rate component, which means we may expect FTX perpetual contracts to trade at a premium relative to other perpetuals with positive interest rate components.

Deribit

Like FTX, Deribit’s funding rate calculation is quite a bit different from BitMEX. Deribit calculates and applies the finding rate in real-time, every single millisecond. Deribit is the only perpetual market with a funding rate that is applied and paid in real time as it is calculated. Deribit uses a 30 second exponential moving average price in its mark price calculations, which places more weight on recent prices.

Kraken

Like Deribit, Kraken applies funding payments continuously. There is an important difference however, in that these payments are made using the funding rate calculated from the previous four-hour period. Like most other exchanges, the premium component on Kraken is scaled so as to have a realization period of eight hours.

dYdX

The dYdX perpetual market design differs from BitMEX’s in a few key ways. Funding on dYdX’s perpetual market is calculated and applied every second, with the funding rate itself updating every hour. By applying funding continuously, we aim to keep the perpetual price as close to the index as possible at all times, avoiding the “basis” which, in other designs, accumulates over the time period leading up to the funding payment. This design was a good fit for us given that we apply funding payments in a decentralized manner via the dYdX Perpetual Protocol smart contracts. Like BitMEX, we include an interest rate component fixed at 0.01% per eight hours, and use a time-weighted impact price to calculate the premium.

Funding Rates as Yield

As we discussed in our article on crypto dollar yields, perpetual contract funding can be a great source of dollar yield for investors and even savers. Positions can be created in which there is no exposure to the underlying price of the cryptocurrency, but the position is constantly earning interest in the form of the funding rate. These are constructed by taking the opposite side of the funding rate and then hedging that exposure through the spot market.

Let’s walk through an example.

Assume that the price of a perpetual market has consistently traded above its corresponding index price over an hour window. In this case, the funding rate for that period will be positive, meaning longs will pay funding to shorts.

A trader who wants to collect the funding rate would open a short position on the perpetual. For this example, let’s assume the price of the perpetual is $10,005 BTC/USD and the index price is $10,000 BTC/USD. Once they enter a short position at $10,005 BTC/USD through the perpetual, they are now exposed to fluctuations in the price of BTC. If the price of BTC goes up, their position will be much more underwater than the funding they’ve collected.

To hedge out of this market risk, the trader can create a position that is “delta-neutral,” meaning changes in the underlying price don’t affect the position’s PnL. In our example, the trader would offset their perpetual short position by going long BTC on the spot market. That way, if the price of BTC goes up or down, the position's dollar value remains the same, while collecting the funding rate every settlement period.

The same trade can also be done in reverse. Let’s say the perpetual was trading at $9,998 BTC/USD and the index price is $10,000 BTC/USD. In this case the funding is negative and shorts pay longs. A trader would enter into a long position through the perpetual and then short BTC on a margin exchange, or even another perpetual market. The trader would have to take into account any interest or funding payments made on account of the short position.

This type of trade is similar to a traditional “cash and carry.” Historically, cash and carry trades on Bitcoin perpetual markets have yielded very high annualized returns, frequently in the double digits. Since capital is needed to go both long and short, leverage can be used to make the trade more efficient. When leverage is applied, the position collects an amount of funding proportional to the notional size of the trade, and not just the amount of collateral. The downside of using leverage is that positions can be liquidated, which can quickly wipe out any funding earned.

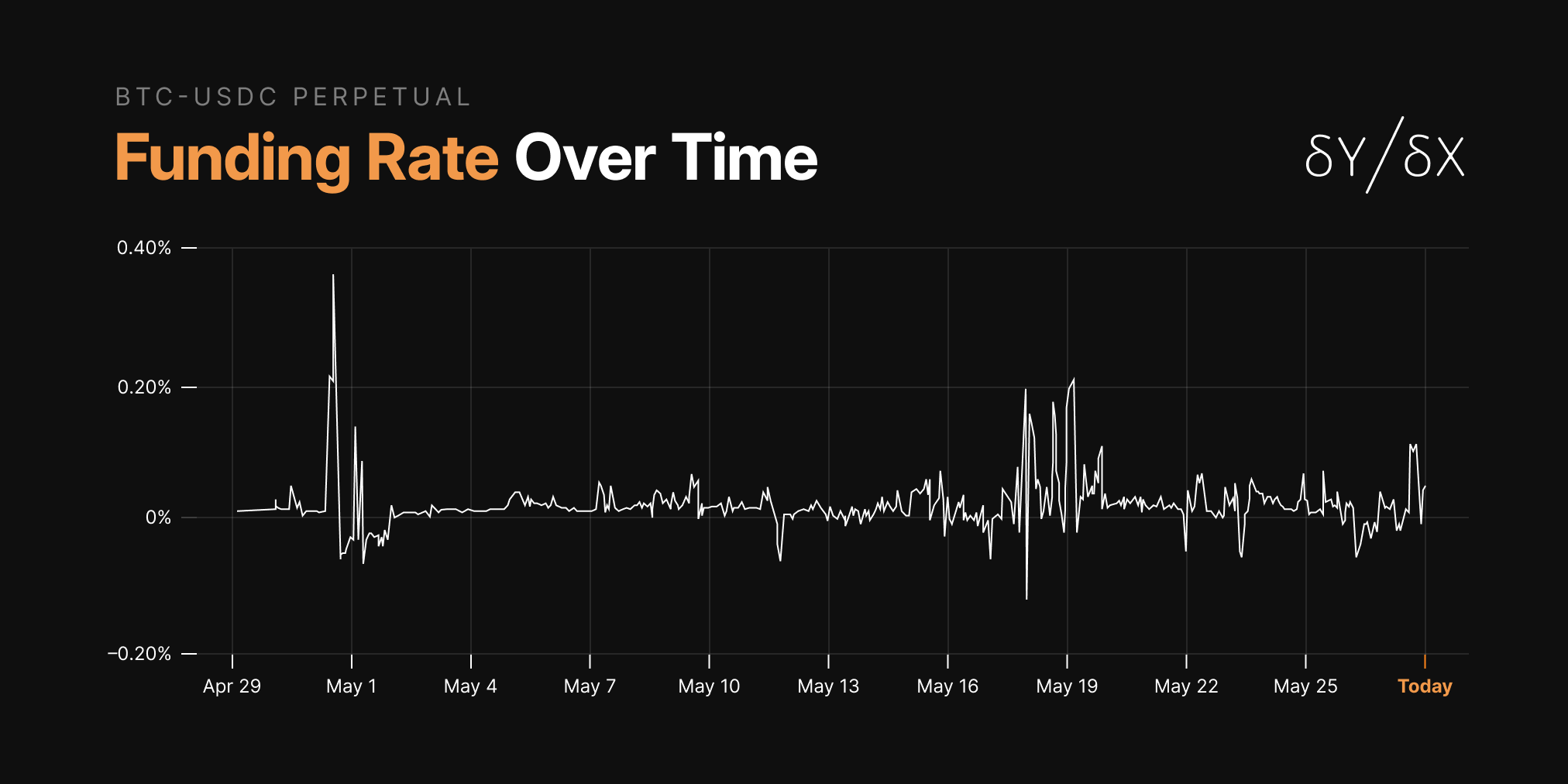

Funding Rates on dYdX

Since its launch, the BTC–USDC perpetual on dYdX has seen a significantly elevated funding rate compared with other stablecoin-denominated perpetual markets. In just 1 month after launching, longs have paid shorts a total of 13% in funding, equal to 156% in annualized earnings.

Why has our funding rate remained elevated?

Our first cohort of traders has been just slightly long biased. As we discussed in this post, when the price of the perpetual is higher than the price of the index over time, the funding rate will be high in order to incentivize shorts to come and take the other side. Over time, it will be interesting to see what type of trader gravitates to dYdX and how our funding rate reacts to that market structure. In the meantime, we’re excited to see more traders coming in to take the other side of the market!

Special thanks to dYdX Engineer Ken Schiller, for his excellent research on the perpetual funding market.

dYdX is the most powerful open trading platform for crypto assets with spot, margin, and perpetual markets.

Start trading on dYdX today and check out our new BTC-USDC Perpetual Market!

You can reach dYdX via email at contact@dydx.exchange, on Twitter, or on our official Discord.