Comparing DeFi Token Models

Introduction

DeFi tokens have recently been far and away the best performing sector in the cryptocurrency markets. The primary reason they have seen such growth can be boiled down to a single factor: they accrue value. Most DeFi token models are designed in such a way where token holders benefit proportionally to network usage and growth. In fact, many of the most popular models operate similarly to traditional equity, in which holders value the asset based on the fees earned by the network as well as the ability to govern it. DeFi tokens also incorporate some form of incentive design to align the interests of the network with long term holders, staking being a popular example. While DeFi tokens have passed the initial value capture test, many of these models can be upgraded. Over time, more experiments will illuminate how to best capture value from a decentralized financial network through a token.

The idea of using tokens to incentivize decentralized network growth isn’t new. Fred Ehrsam’s early blog post on the decentralized business model described how a token could be used to help solve the proverbial chicken and egg problem faced by networks and marketplaces. The problem with this early implementation was that there was no way to distinguish speculators from long term investors or users committed to the network. We saw this play out during the 2017 ICO bubble — tokens were sold off to speculators who quickly flipped them for a quick profit, leaving the actual networks completely behind.

Since then, the industry has been able to experiment with token models designed to create multi-sided networks with long-term focused participants. DeFi in particular was a perfect breeding ground for this experimentation because the general utility of the sector like staking, lending, and borrowing meant that new users were joining networks, which created a larger sample set to test token incentives with. As a result of this experimentation, three distinct token models have emerged, but it’s also very common for tokens to combine features.

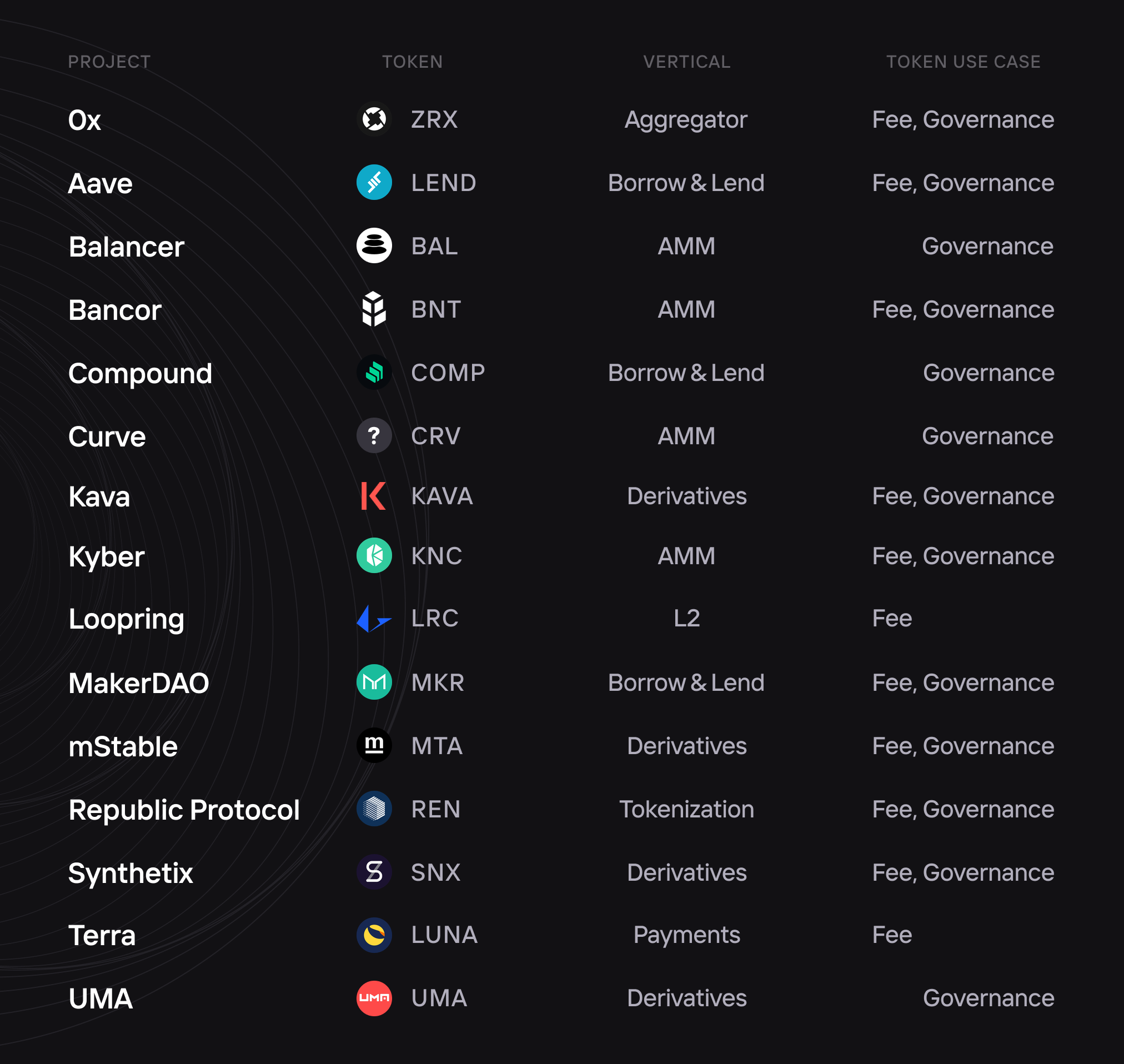

- Fee Tokens (cash flows)

- Governance Tokens (governing rights)

- Collateral of Last Resort Tokens (system re-collateralization)

Interestingly, many of the most successful tokens incorporate both functionalities. Many tokens also start off as governance tokens and then look to add in some type of fee capture only if token holders vote for and approve it. This also has implications around the regulatory classification for many of these tokens. Naturally, we can expect network participants to push for more value capture.

Token Classification

Fee Tokens

Fee tokens are tokens which have a cryptographically verifiable claim on fees generated by a DeFi protocol. Fees are typically baked into accessing and using the DeFi protocol — very similar to transaction fees charged by traditional financial service providers. These fees can be passed directly to the Ethereum address that holds the underlying fee token or into an omnibus wallet architecture. So far, fees have been distributed either in stablecoins, an underlying network token, or in ETH.

In some instances, token holders can vote on how to use the fees accrued to them. In the case of Kyber Network, token holders can use their funds to buy back KNC on the open market and burn them out of the supply. Buy & burn’s are a frequently used feature for deflationary DeFi tokens to accrue value.

Fee tokens are a big step forward for DeFi token models because they can be valued on the basis of cash flow. This makes it easier for investors to reason about valuation relative to the various intangible factors used to value hard-capped, fixed issuance money assets like Bitcoin and Monero. Now, tokens can be valued on the basis of their future cash flow, and can be compared against one another to identify mispricing amongst projects building for similar use cases.

Governance Tokens

Governance tokens are those which give holders the ability to vote on how the project’s underlying smart contracts function. The rationale behind the value of governance tokens is that a fully decentralized protocol shouldn’t be owned by anyone. Token holders are intended to collectively own the set of contracts and to decide how they change over time.

So far, DeFi tokens supporting governance have been used to vote on proposals around which assets are supported, collateralization levels for certain assets, and where protocol fees should be directed. For example, Compound has received an influx of new proposals recently for deciding how much value can be borrowed against certain assets.

Over time, governance will shift towards deciding over how smart contracts are upgraded. This will be done programmatically: once a vote is confirmed, smart contracts can adapt without human intervention. To do this, developers would need to include finished code along with their proposals, so the smart contracts can automatically integrate it once voting is complete.

Collateral of Last Resort Tokens

Collateral of last resort tokens are tokens that act as backstops to a price peg that a DeFi protocol attempts to maintain. For protocols in which synthetic assets are created, there can be situations where there is not enough external collateral to restore the peg of a synthetic asset. In this case, the underlying network token can be used as a source of liquidity to buy and/or sell assets required to restore any peg. In exchanges for serving as the protocol’s backstop, holders of collateral tokens are usually rewarded with a share of network fees.

Two of the most prominent examples are MKR and MTA. MKR was the first token model to pioneer the collateral of last resort functionality. If for any reason the system becomes uncollateralized, MKR is sold on the open market to backstop the Dai supply. With MTA, if any of the stablecoins within its basket lose their peg, MTA can be sold to make sure stablecoin depositors are made whole.

Staking and Inflation

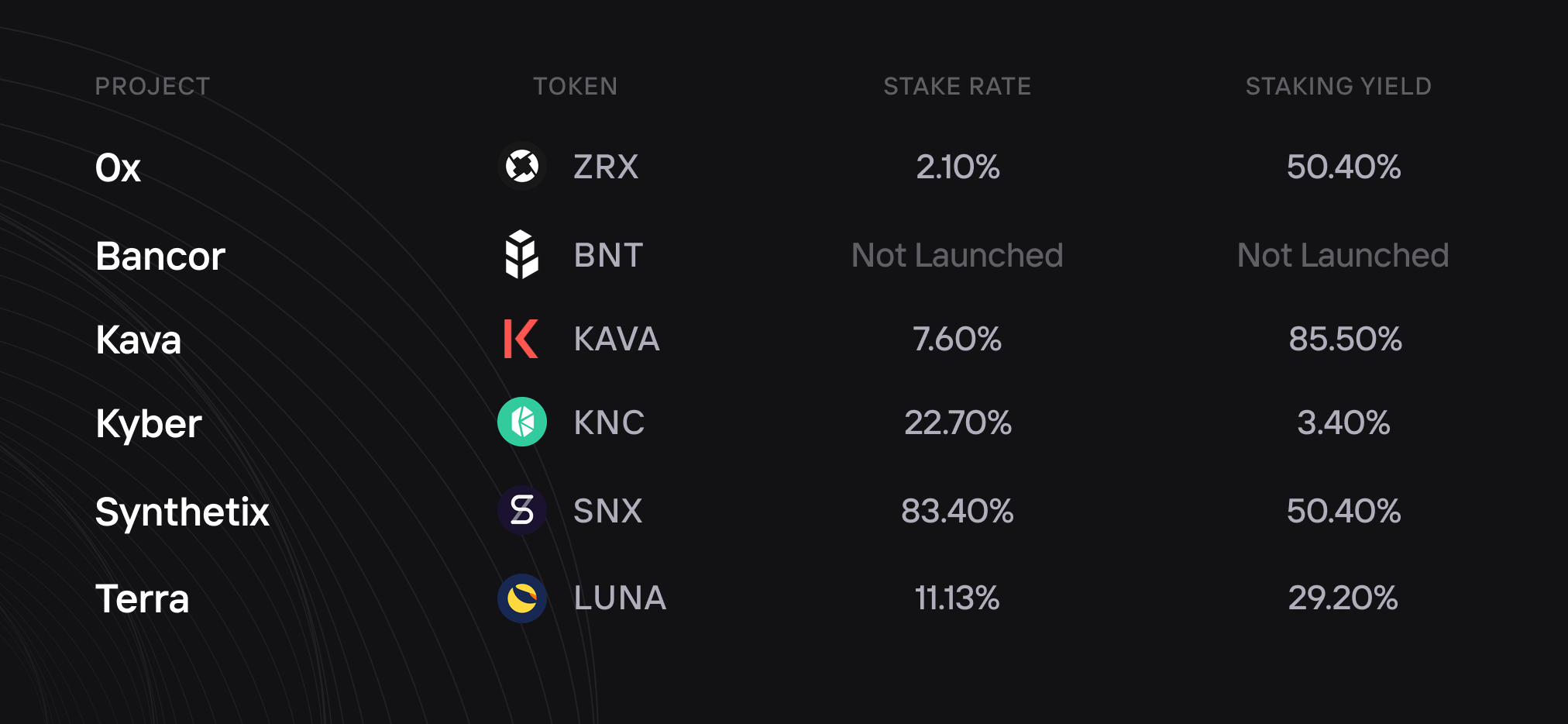

Two elements present in many DeFi token model implementations are staking and inflation.

Staking is used to align holders with the long term interests of the protocol. Through staking, holders lock up their assets for the future, effectively removing them from the circulating supply so fewer tokens can be sold. More importantly, users often stake for the right to provide a service to other participants in the network. In exchange for providing this service, and in effect making the network more valuable, stakers are rewarded via inflation.

The inflation funding model has proven to be quite successful for bootstrapping liquidity in the earlier days of a protocol. For example, Synthetix used inflation to incentivize stakers to create synthetic assets and then seed Uniswap with them so that there were liquid secondary markets. This culminated in the sETH pool being one of the most liquid places to trade ETH on Uniswap.

Staking also has a particular effect on market structure, and whether or not it is beneficial is up for debate. In general, staking yields, and specifically high staking yields create negative pressure on liquidity, making it difficult for buyers and sellers to transact without having a large effect on the price.

There are two reasons it dampens liquidity:

- Staking yields increase borrow costs

- Holders are incentivized to stake and keep assets off exchange

High borrow costs make it difficult for market makers to acquire the inventory required for a two-sided market. The fees they can earn by providing liquidity can’t outperform the fees required to compensate holders on their forgone stake, especially early on in a network’s cycle when the inflation rate is highest. Similarly, high borrowing costs deter short sellers because their expected return would have to cover price depreciation and the staking yield. Given the recent price action of DeFi projects, it’s very unlikely that many short sellers are going to play in this market. Another side effect of high staking rewards is that holders are somewhat disincentivized to keep their assets on exchange.

Low liquidity can lead to high volatility, and in the case of many high promising DeFi tokens, it’s upwards volatility. DeFi tokens that actually accrue value almost always have a bullish market structure because there are so few sellers. This makes DeFi tokens very convex — a great great example is SNX.

Value Capture

The most novel feature DeFi token models bring to the crypto space is the ability for a token to have intrinsic value.

Prior to DeFi tokens, very few token models could be valued on any quantitative basis. The first generation of crypto assets in general weren’t valued, they were priced, and market participants would primarily react to market structure and narratives. This fundamental gap in intrinsic value is what made the crypto markets so speculative and volatile. Once it was broadly discovered that those assets could only accrue value by having strong holders, exchanges launched pseudo equity tokens in which earned revenue was used to buy back and burn tokens, effectively mimicking a dividend. Exchange tokens were a bit flawed in that the buy and burn process was not transparent. Holders had no idea if purchases were being front run or if purchases were even happening at all. So far, exchange tokens leave much to be desired in terms of value accrual.

With DeFi tokens, protocol fees directly accrue to token holders, so network value can be analyzed through basic frameworks like Discounted Cash Flow (DCF) at minimum. A valuation can be derived from forecasting out future network growth and then reasoning through what it should be worth today. Additionally, DeFi platforms are unique in that they usually need to bootstrap a supply side to sufficiently serve the demand side. To do this, many token models incorporate staking and inflation rewards (as mentioned above), which means holders are incentivized to keep tokens out of circulating, creating a dampening effect on selling, which in turn leads to greater value capture.

DeFi tokens with purely governance capabilities are a bit different in terms of value capture. Based on first principles, the value of a governance token should equal the marginal cost to fork the network. DeFi networks are different in that forking the code doesn’t necessarily mean you can fork all of the liquidity away, which is the defining moat within DeFi. Given this, the market is likely placing some premium on governance, even more so for completely community run projects like Yearn Finance. Since launching, Yearn has performed much better than COMP and BAL, two of the other most dominant governance tokens.

(source: coingecko.com)

Bootstrapping with Liquidity Mining

Another area where DeFi tokens have really innovated is liquidity mining. As we mentioned in our latest edition of dYdX Trader Insights, liquidity mining is a novel way for DeFi protocols to bootstrap liquidity and build a user base. Liquidity mining is similar to Bitcoin mining in that protocol issues rewards to supply siders who provide work, or in the case of DeFi, liquidity, which makes the network more valuable for the demand side. It’s this incentive that helps create the initial network effect.

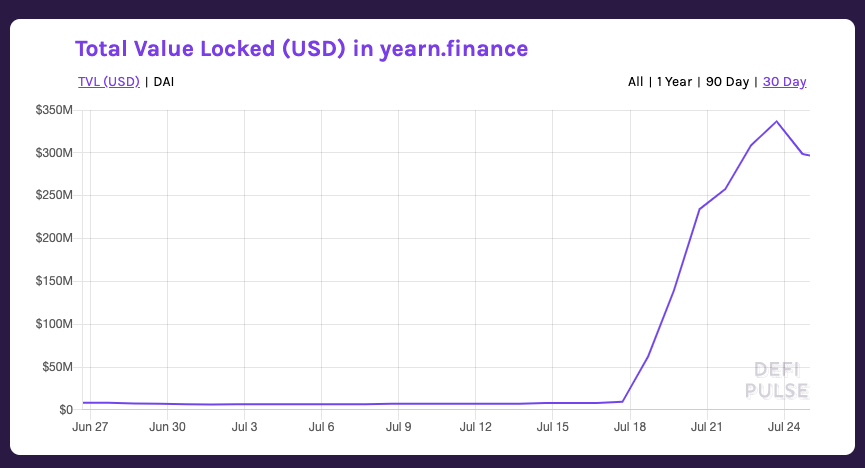

Even with liquidity mining being so new, it has been a success based on a number of early launches. Compound saw massive growth in deposits after it launched COMP liquidity mining, on the order of 400%. Similarly, Balancer’s active users have skyrocketed since they announced BAL mining. Lastly, as has been the main talking point in the crypto markets over the last week, Yearn Finance saw astronomical growth in users and in total value locked on the back of their YFI token launch. Total value locked in Yearn’s contracts have ballooned from just under $10 million USD to nearly $300 million USD in the span of a week,

While liquidity mining has clearly been an effective way to bootstrap growth, a lot of the activity is self-referential, meaning it’s a lot of the existing DeFi money shuffling between the best yield opportunities, and also using DeFi protocols to obtain leverage. This doesn’t mean that liquidity mining is unsustainable, but it’s important to acknowledge two realities. First, users are locking up funds in these protocols for the most part because of the yield. If the liquidity mining opportunity wasn't available, it’s much less likely for protocols to have this much value locked in them, which also affects their intrinsic value because they would be earning less fees.

Second, since a lot of these liquidity mining opportunities are denominated in stablecoins, users are taking on leverage and using a portion of their rewards to pay off interest — in principle, a good trade, but it creates a lot of risk. The issue here is that in times of volatility, DeFi can be very fragile, and this leverage can be unwound quickly. Unfortunately, liquidity mining will likely grow leverage within the system, so it’s important to be cognizant of the risk and discounting that when allocating capital to liquidity mining.

Conclusion

DeFi token models are a huge step forward for the crypto ecosystem for a number of reasons. First and foremost, DeFi tokens have intrinsic value via the on-chain fees they earn from the protocol. This makes it much easier for investors to coordinate around the value of these tokens rather than having to price tokens based on market structure and sentiment. Secondly, DeFi tokens are used as incentive mechanisms so that network participants act in ways that reinforce a protocol’s network effects. In DeFi, tokens are mainly used to incentivize liquidity, for which early contributors can earn very high yields. Based on a number of new launches, these liquidity incentives seem to have a very meaningful impact on network effects.

Luckily, we are still at the precipice of DeFi token experimentation. The initial uses — fees, governance, re-collateralization — are strong uses of a token, but we believe the stage is set for even more innovative uses. As DeFi networks grow, new token use cases will be implemented to maintain many of the network effects being created today.

If you’d like to get started with trading on our platform or have any other questions, please join our Discord and follow us on Twitter.

Trade on dYdX now →