Trader Insights: Yield Farming

This is episode #02 of Trader Insights, a series on trends & strategies for trading cryptocurrency.

A new way to build network effects and liquidity in crypto

One of the earliest beliefs within the Ethereum community was that native tokens were an excellent way to bootstrap network effects. While the idea of early network users owning equity was powerful, the actual implementation was blown out of proportion during the 2017 ICO boom. During that time, token holders were much more focused on speculation than building the underlying network. More recently, decentralized finance protocols have been using new token incentives to drive liquidity and users to their platforms. Formally dubbed “liquidity mining,” decentralized finance protocols have been designed to reward their users with native token that can be used as both a cash flow and governance asset.

The first decentralized finance protocol to utilize liquidity mining was Synthetix. SNX holders that turned their sUSD into sETH and contributed to the Uniswap sETH pool were rewarded with more SNX. The experiment was successful — sETH became one of the most liquid assets on Uniswap. Compound’s most recent COMP launch was the next protocol to launch liquidity mining, and based on early indications, it has been a massive success. When COMP first launched, the protocol had roughly $100 million USD in assets locked in the protocol. Now, the protocol boasts nearly $1 billion USD in locked assets, just two weeks after launch.

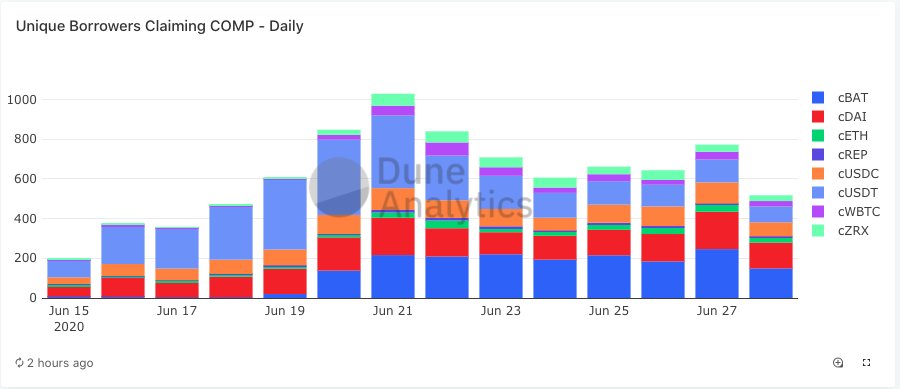

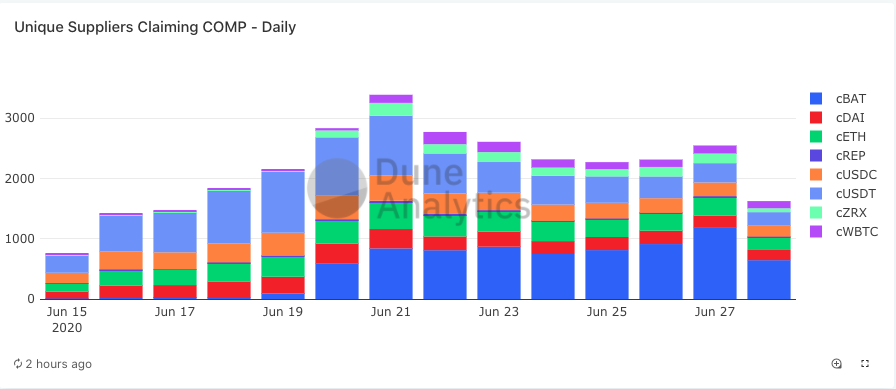

It’s clear that liquidity mining is a great way to bootstrap network effects, which for decentralized finance protocols means liquidity. Diving into Compound’s numbers post COMP launch, over 2,000 unique suppliers and over 800 unique borrowers have been collecting COMP daily.

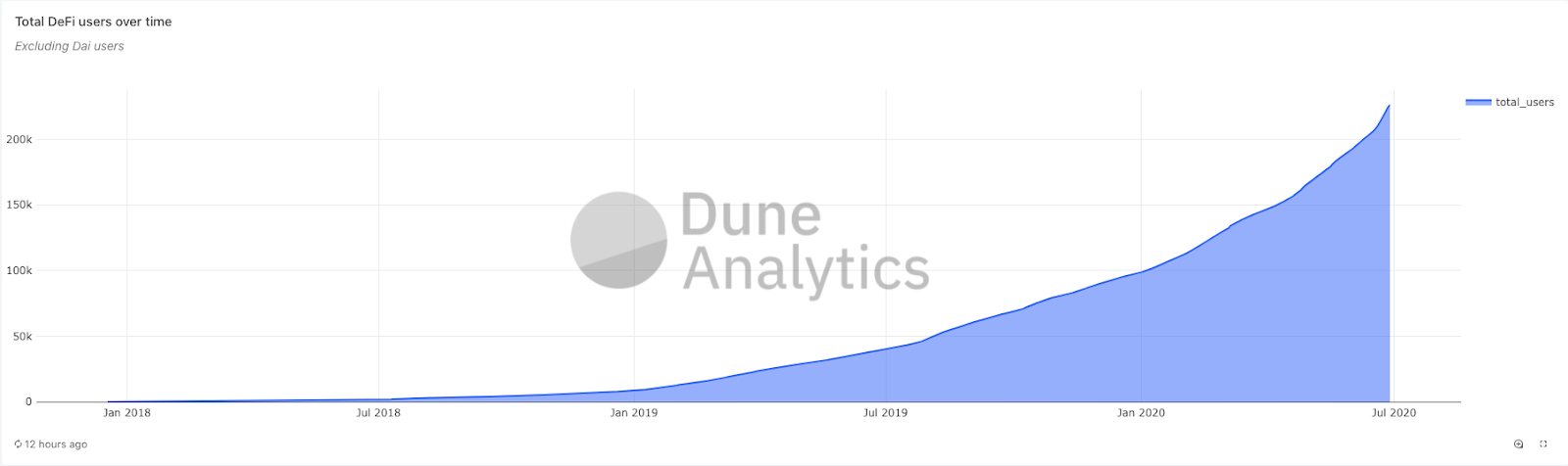

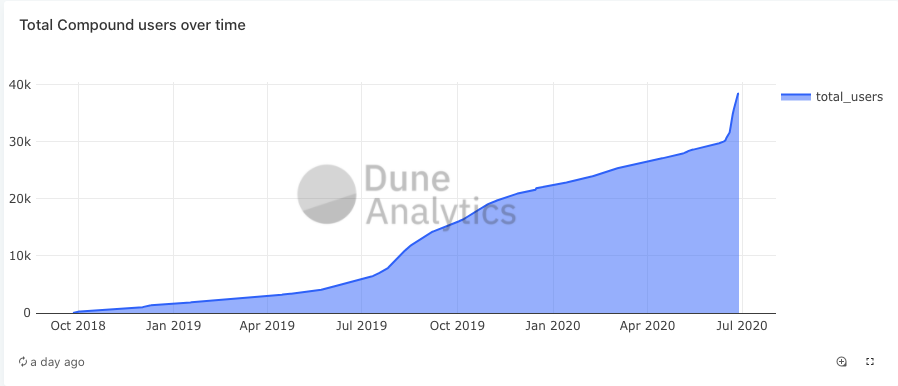

In terms of unique users, the COMP launch increased total uniques from 30,000 to 40,000, over 30% increase in two weeks. When comparing Compound’s unique user growth with the DeFi more broadly, it’s clear that liquidity mining through COMP was an effective way of growing users.

An important aspect of liquidity mining is that it gives decentralized finance protocols a way to compete with larger centralized platforms. For one, liquidity mining can actually pull idle assets out of exchanges and into DeFi protocols. Assuming those idle assets aren’t earning any interest, liquidity mining is extremely competitive to centralized exchanges. Second, liquidity mining drastically reduces the costs associated with spinning up new maker/taker books. Decentralized finance protocols using liquidity mining can be much more efficient than centralized venues in going to market with new products quicker.

Liquidity mining also won’t be unique to a single DeFi protocol. Soon after COMP launched, Balancer protocol began its BAL mining incentive program. Similarly, Synthetix announced a liquidity mining partnership with REN protocol and Curve to build liquidity for tokenized representations of BTC on Ethereum. Given the success of these launches, it’s very likely we may see a liquidity mining boom in the same spirit as the 2017 token boom.

While liquidity mining induced growth is good for DeFi protocols, nothing ever lasts forever. It’s no surprise that users and assets grew as the underlying price of COMP increased. If Coinbase never announced their intention to support COMP, it’s unclear just how high user growth and total value locked would have reached. It’s important to distinguish network growth that’s strictly tied to speculating on the underlying token rather than users wanting to accumulate the token over the long term.

Market Roundup

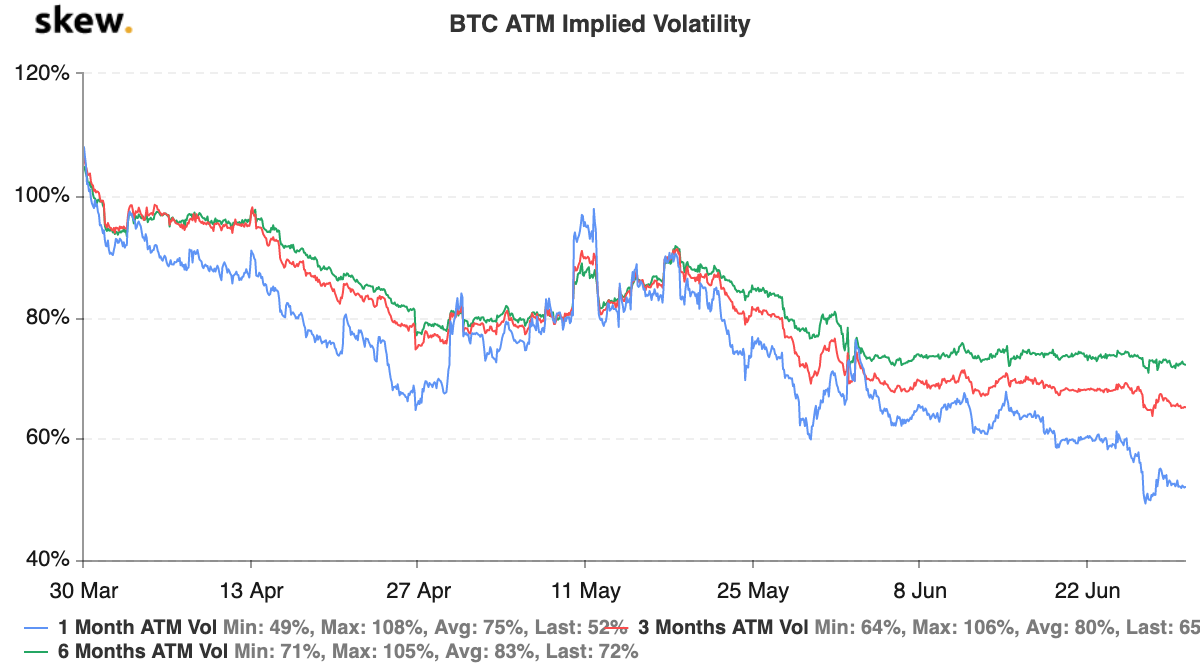

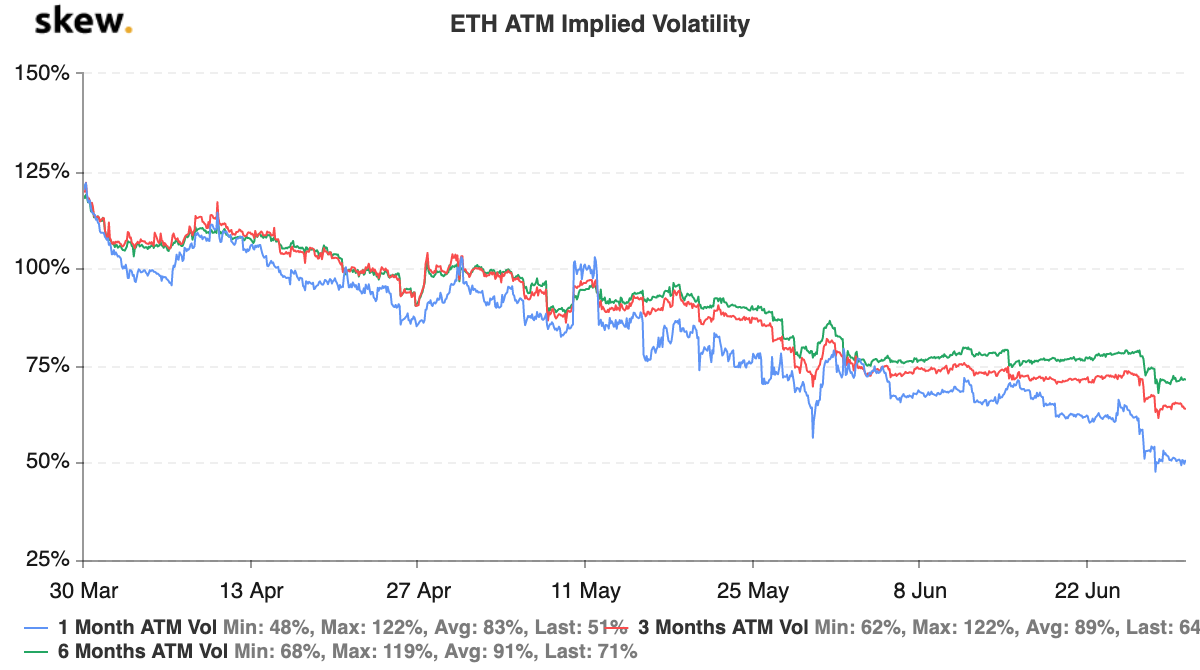

A prolonged low volatility regime: Both BTC and ETH vols have been muted since the halving. This makes sense given the hype around the event, but both BTC and ETH have remained silent in the face of new fundamental catalysts. Even more unique, ETH implied volatility has fallen below BTC implied volatility. Given ETH has historically been much more volatile than BTC, this has caught a lot of the trading community off guard.

There’s a couple of reasons for this low vol regime. First, miners have likely been more active hedgers since the halving — working with finance firms who build them structured products to offset risk and capture yield. Many of these products involve some form of yield harvesting that comes from selling volatility. Second, an interesting theory shared by Genesis Volatility is that a lot of the ICO projects with large ETH treasuries have been monetizing their holdings by selling volatility.

Regardless of what’s causing such low volatility, historically, volatility has spent little time at these levels.

DeFi derivatives: Derivatives exchange FTX has launched a number of new DeFi focused trading products. The big release was a new DeFi index comprising a number of the highest market cap assets. This came after a secular DeFi uptrend which we discussed in our previous issue of dYdX Trader Insights. Along with the DeFi index came individual markets for COMP and BAL.

A week after launch, the DeFi market has roughly $1 million USD worth of open interest, while COMP and BAL have $3.5 million and $250k in open interest respectively. Not surprisingly, all of the associated perpetual markets have a negative funding rate, indicating there is more short interest than long interest. Performance wise, the DeFi index has come down a bit, but is still trading much higher from its launch price.

The return of decentralized betting: The crypto ecosystem has long fantasized about truly decentralized betting markets. Over the coming weeks, two DeFi protocols, Synthetix and Augur will be launching betting markets. Synthetix is unique in that they’re releasing parimutuel binary options. These markets allow speculators to trade events based on binary outcomes. For example, will BTC trade above $10k on or before July 31st 2020? Augur, on the other hand, aims to be a more robust no-limits betting platform where any arbitrary market can be created. This is an exciting space to watch and we’re expecting strong volumes for their respective launches.

First Derivative

Second Derivative

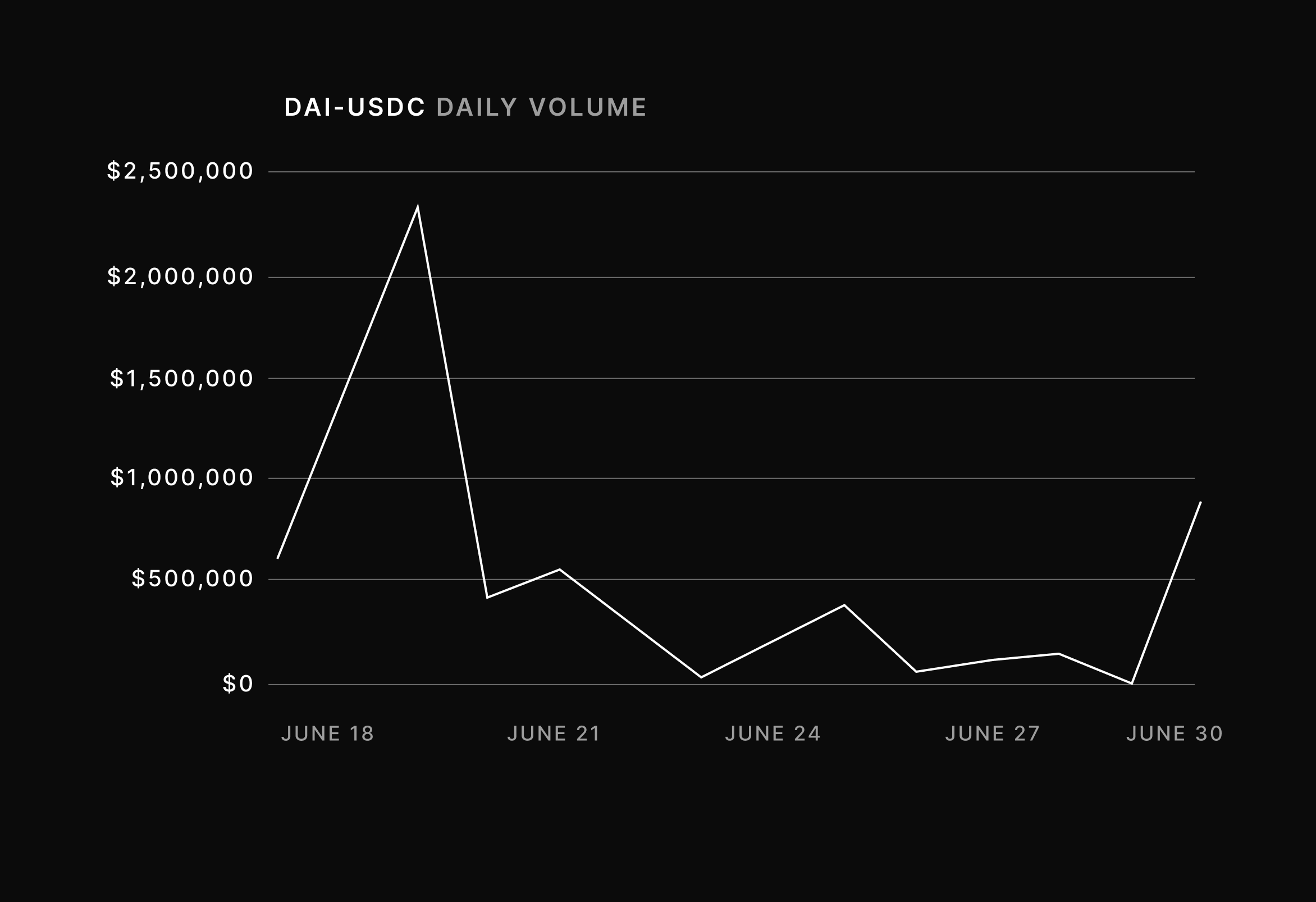

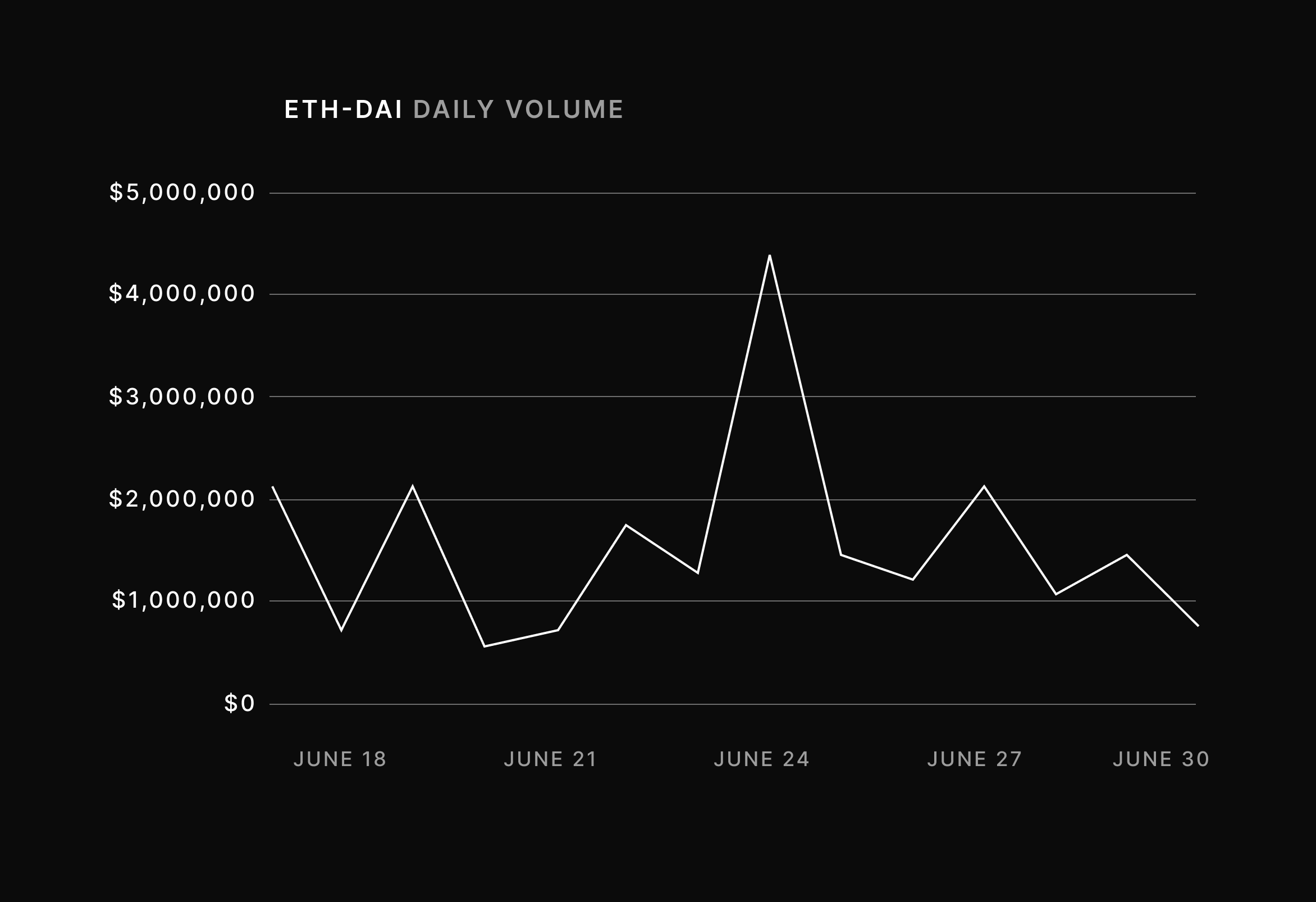

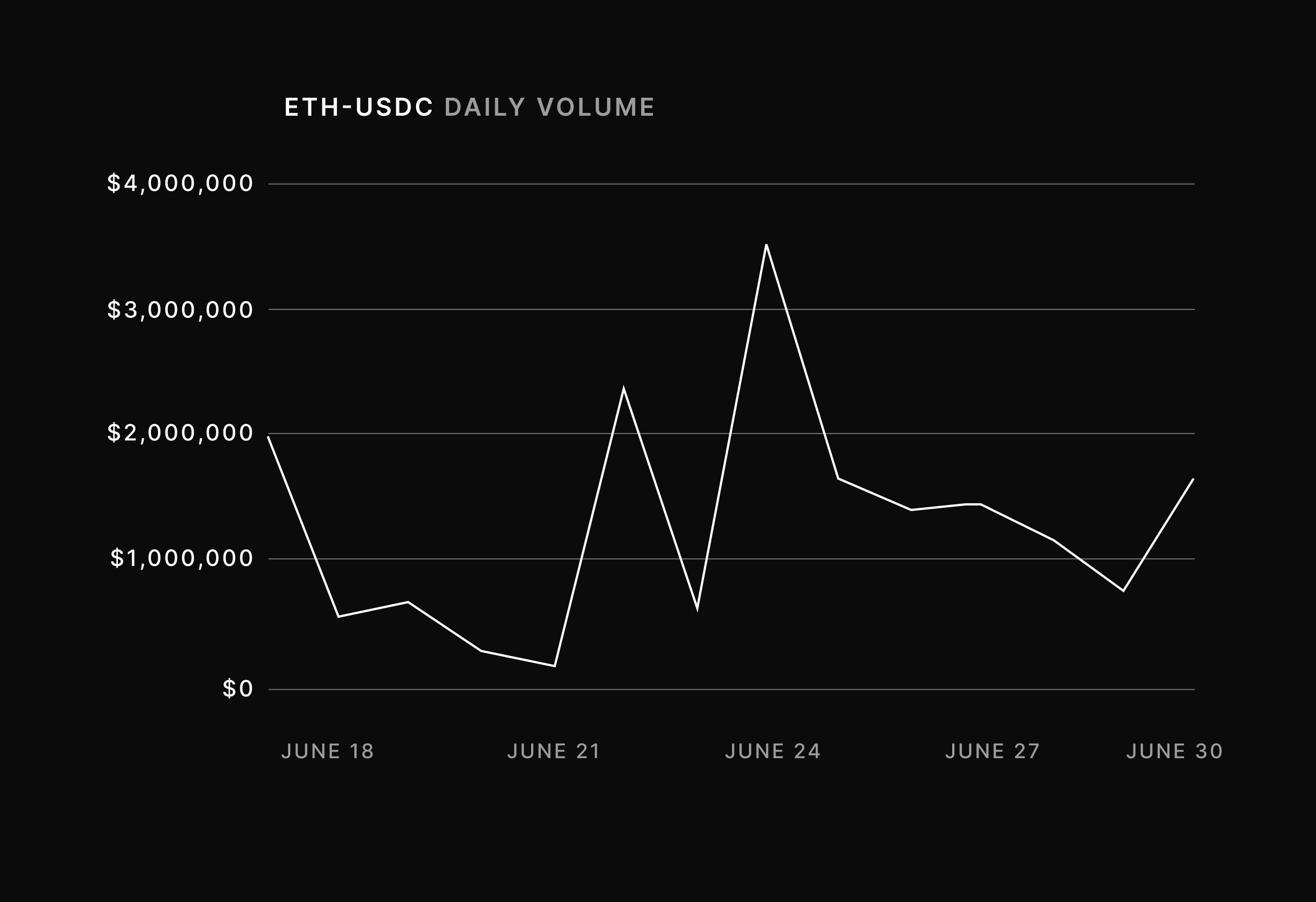

Over the last two weeks, we saw the most flow in ETH<>USDC, with DAI<>USDC being a close second. Liquidity has improved on our ETH<>USDC so that most likely became our preferred venue to get ETH exposure. Based on everything happening with yield farming, we attribute the increase in DAI<>USDC volume to users swapping stablecoins so they can capture various yield opportunities.

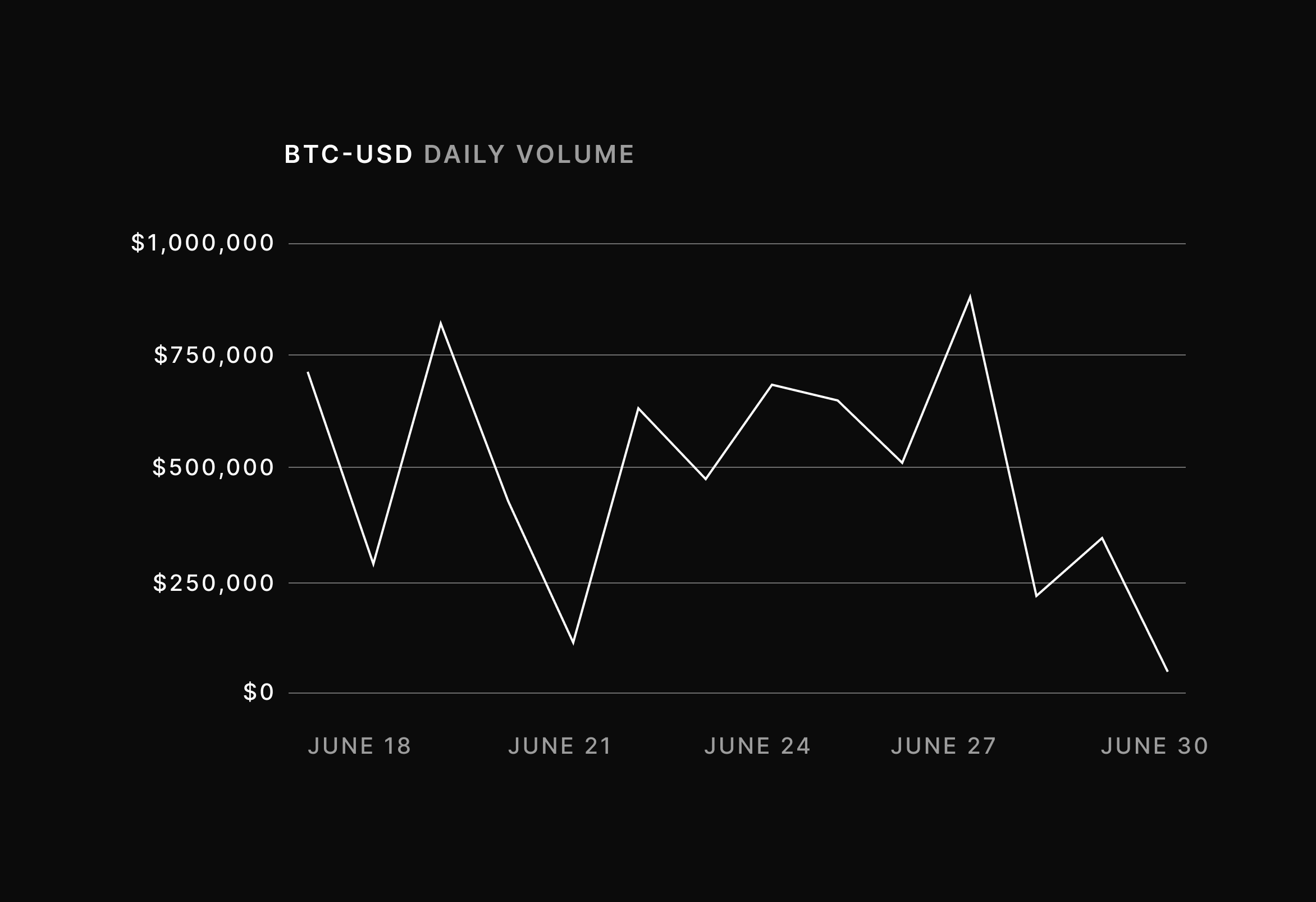

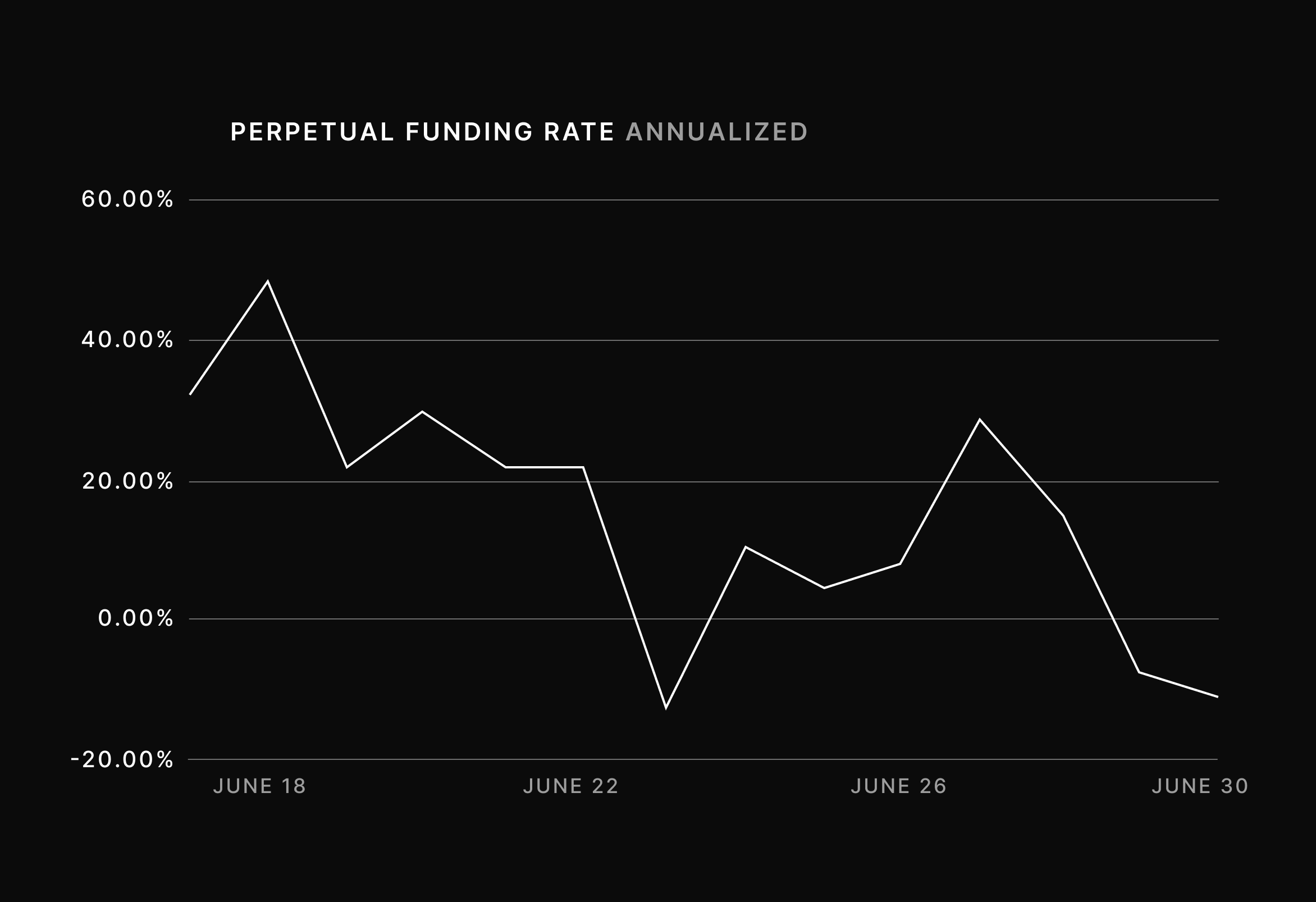

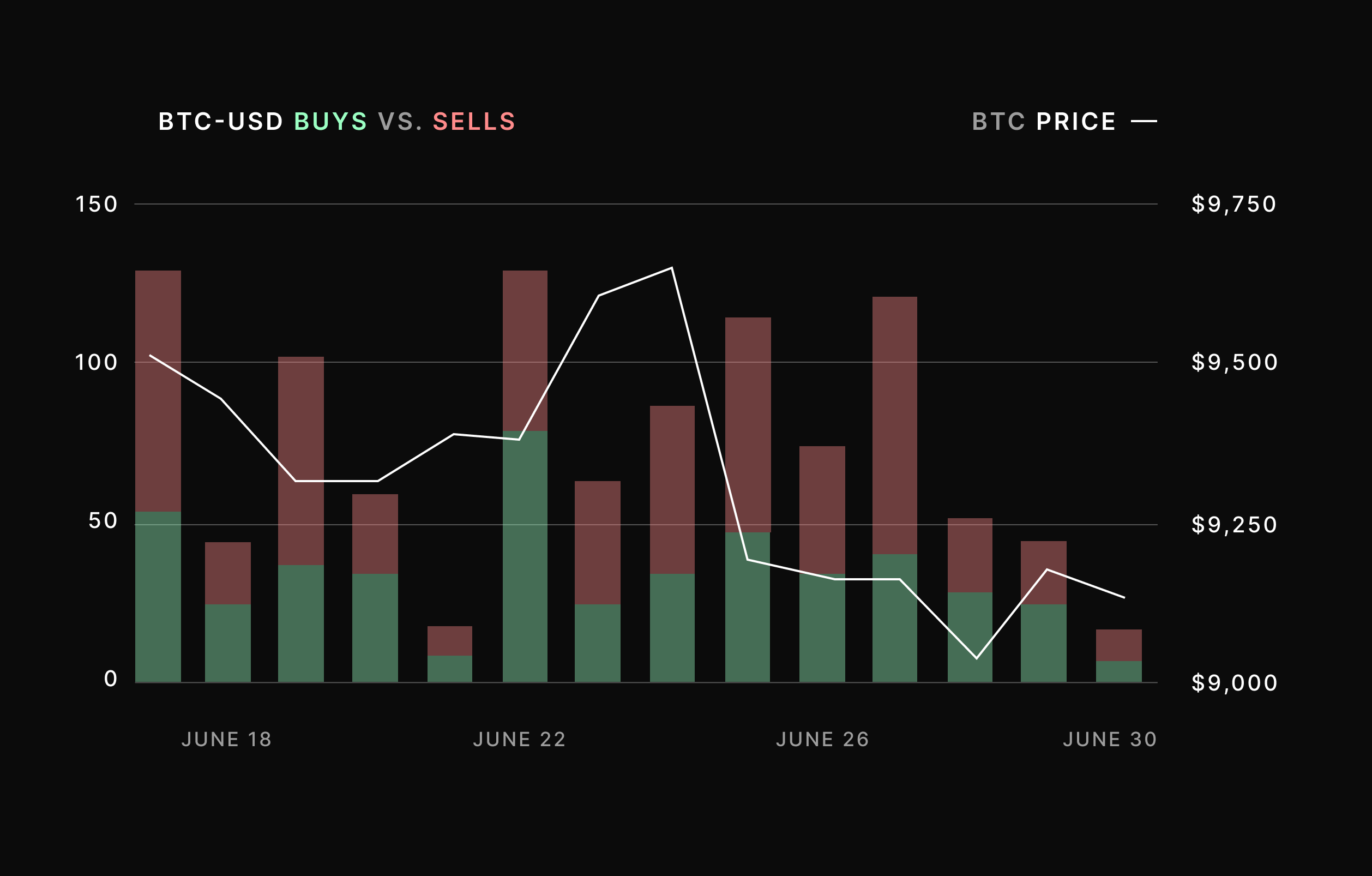

BTC volatility has remained low for quite some time, but we saw much more selling than buying on the BTC<>USDC perpetual. This is in line with BTC’s price decline and we’re also seeing more delt neutral traders on our swap that are collecting funding. More delta neutral swap traders is also evident by the drop in the perpetual’s funding rate, moving from just at 40% apr down to -10% apr by the end of the two week period.

Around the Open Financial System

- Curve Finance released a formal spec of their CRV governance token and the Aragon DAO it will govern. Also included in the whitepaper is an overview of how votes will be weighted in the DAO. Curve’s system is unique in that votes are weighted both by total stake, but also for how long CRV tokens are stored in time-locked contracts. Curve is the first DeFi protocol to require governance participants to time-lock their tokens.

USDT surpasses $10 billion in total market cap

- Tether continued its ascent as the cryptodollarization trend captures more of the crypto market cap. As we discussed in our piece on crypto dollar yields, stablecoins are the center pieces to a whole new class of financial instruments and most importantly, these instruments allow their holders to earn dollar yields not available in the traditional world. This most recent spike in issuance has been a direct result of DeFi offering these large yields.

- A vulnerability was found in Balancer Protocol shortly after it launched in which an attacker could use a flash loan and then trade that principle within a specific token pool. In this specific exploit, an attacker actually borrowed funds from our exchange and then traded within the STA/STONK pool, manipulating the price of the pool so that they could swap assets at a much cheaper price.

We wrote about our integration with Curve Finance

- We released a tweet thread that went into a bit more depth about our recent integration with Curve finance. We’re excited about it for a couple of reasons. For one, by utilizing Curve, we’re giving our users the most liquid way to access stablecoin liquidity. Second, using Curve is a much more seamless user experience compared to swapping between stablecoins across fragmented DEXs.

dYdX is the most powerful open trading platform for crypto assets with spot, margin, and perpetual markets.

Start trading on dYdX today and check out our new BTC-USDC Perpetual Market!

You can reach dYdX via email at contact@dydx.exchange, on Twitter, or on our official Discord.