Examining the World of Crypto Dollar Yields

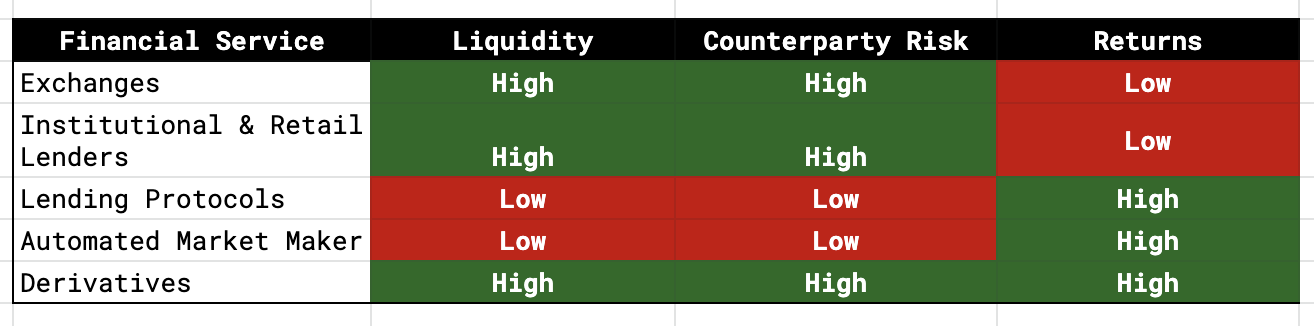

The ability to earn dollar yields that are multiples higher than what most investors can earn in the traditional financial system has been, and will continue to be, one the largest drivers of new demand for cryptocurrencies. These yields are a function of both demand for dollars in the crypto economy as well as the difficulty associated with getting fiat into the ecosystem. The most widely used financial services that produce dollar yields are exchanges, centralized lenders, open finance lending protocols, automated market maker models, and crypto derivatives. Each of these venues is unique — they vary based on a number of different factors including liquidity, counterparty risk, custodianship, and of course, potential returns.

One aspect many of these platforms share is that they are powered by crypto dollars. Crypto dollars come in many shapes and sizes, which this post will dive into later, but the general premise is that it’s a digital asset which pegs its value to the dollar. The most novel aspect about these crypto dollars is their programmability, they can be sent anywhere in the world and can be seamlessly integrated into any blockchain-based financial application. An interesting parable is to think of crypto dollars as Venmo dollars that were set free — finally able to be used within other financial applications.

The most notable aspect of crypto dollar yielding opportunities up to today has invariably been how much greater they are than traditional counterparts. As an example, the US 1 year treasury note yielded 2.57% in 2019, while lending USDC on dYdX yielded 4.86% apr over the same timeframe. This premium is a function of the fact that crypto markets have historically been bullish, but even more importantly, they reflect how hard it is to actually get dollars into the ecosystem. Investors in need of dollar financing know how quickly crypto prices can move so they have been more than willing to pay a premium to get quicker liquidity.

In the early days, the only way to borrow or lend dollars within the crypto confines was through Bitfinex’s margin order book. Yields fluctuated massively as it was difficult for crypto exchanges to secure banking partnerships. Lack of banking made it very difficult for supply to enter the marketplace so there wasn’t much of a neutralizing force when demand suddenly increased.

In order to solve their banking issues, Bitfinex created Tether in 2014. With Tether, dollar representations could be sent within the crypto ecosystem, investors could use it to trade against cryptocurrencies, and those without access to traditional banking could actually hold Tether to get exposure to the dollar. Then in 2017, the market capitalization of Tether ballooned by 1400% (!) as it became obvious that on-chain dollars were far more efficient than having to deal with the traditional system. From then on, the era of the stablecoin took hold.

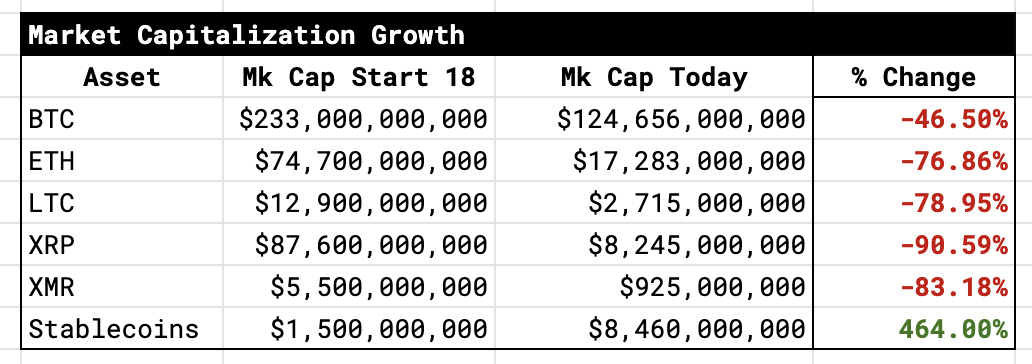

In terms of growth, stablecoins have been by and large the fastest growing crypto asset since the start of 2018, right before many of them launched. Over the course of roughly the last two years, the market capitalizations of the highest market cap assets fell anywhere between 46% and 83%, whereas the market capitalization of all stablecoins increased by 464%.

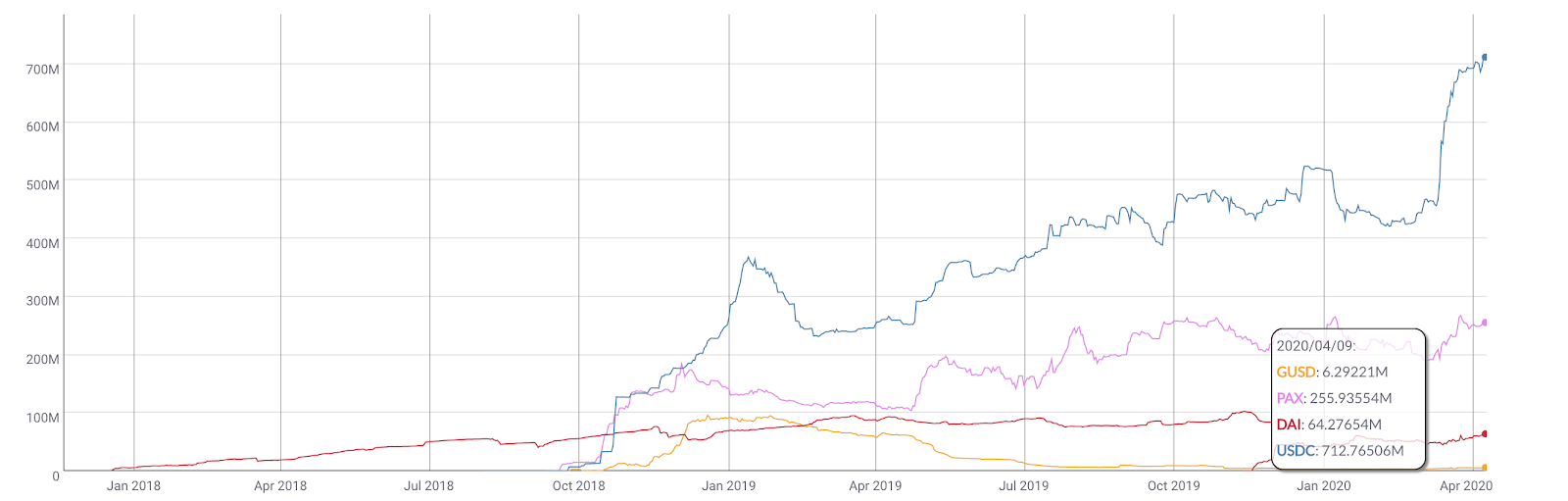

A lot of this growth can be attributed to the fact that many new lending markets were built around these stablecoins in 2018, which enabled them to be lent at a high interest rate. High interest rates created a huge incentive to convert traditional dollars into crypto dollars, as evidenced by the market capitalization growth of USDC, Dai, Pax, and GUSD, the primary stablecoins with lending markets at the time.

On a macro level, interest rate conditions in the traditional system have drastically reduced the opportunity costs associated with holding dollars in a regular bank account. There’s not much interest being lost by turning dollars into crypto dollars. Since the start of 2018, the 10 year treasury yield fell from 2.40% to 0.73%, a 70% decline in savings potential. And that’s just in the United States. In European countries like Germany, the UK, and France, 10 year notes yield -0.36%, 0.30%, and 0.09% respectively. The world has never been this desperate for yield.

Crypto dollar yields aren’t completely immune from a low interest rate world. Following the market decline on March 12, lending rates for USDC fell over 80% on the month from ~4% apr all the way down to 0.45%. Luckily, rather than react directly to central bank policy, crypto dollar yields are primarily a function of market sentiment. If crypto markets can remain uncorrelated to traditional markets, there’s a good chance crypto dollar yields will continue to be much higher than anything offered in the traditional world.

Apart from basic stablecoin lending, there are a number of more complex financial instruments that enable crypto dollar yields. With more complex financial instruments comes the opportunity of higher gains, but of course, with higher risk.

In this post, we look at the most widely used avenues in the crypto ecosystem through which users earn dollar yields, the tradeoffs and risks associated with each venue, as well as the potential returns.

Exchanges

Speculation has been far and away the most in demand use case for nearly the entirety of crypto’s existence, and as such, exchanges have been the biggest beneficiaries of the ecosystem’s explosive growth. As exchanges looked for ways to expand their businesses and find revenue streams less correlated to volatility, it quickly became obvious that the winning business model was to build a vertically integrated crypto bank. They already owned the user relationship and the assets, the next step was to offer them a full suite of financial services. After all, crypto is all about new forms of money.

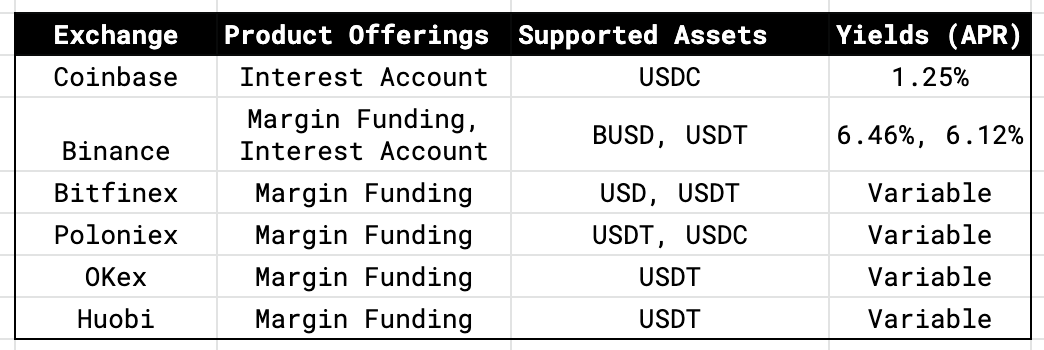

Naturally, extending users the ability to earn interest on their assets is a low lift for exchanges. Users by and large choose to hold their assets on-platform and exchanges already have the demand side necessary to facilitate borrowing. The most common interest earning opportunities available on exchanges are margin funding pools, where users lend their assets to speculative traders, or interest accounts, where the exchange guarantees the user a certain yield and then has the freedom to try and lend those assets out for a higher rate. The former is just like margin funding in the traditional world and the latter is more like a CD.

Lending through an exchange is arguably the most simple way to earn interest on crypto dollars. Since users aren’t required to do anything more than send funds to their address, the experience is very akin to traditional banking, something most users are familiar with.

Liquidity for margin funding accounts is typically high, albeit there could be instances in which all consumer deposits are being utilized. On the other hand, interest accounts usually entail a lock up for a certain period of time. In terms of counterparty risk, exchanges are large central points of failure as they have ultimate custody of user funds. Users lending through exchanges should be cognizant of potential attack vectors and practice diversifying their lending activities away from one exchange. There are also new exchange models, of which dYdX is one, in which the actual exchange never takes custody of users’ funds while they’re being lent. From an overall risk perspective, exchange lending is relatively low, which leads to a lower potential return profile. However, many times the lending yields offered on exchanges are much higher than any consumer savings account, making them worthy alternatives for the risk taken.

Institutional and Retail Lenders

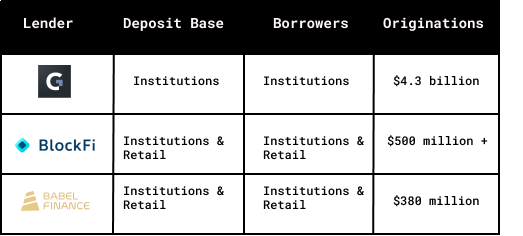

Credit markets have been one of the fastest growing parts of the cryptocurrency industry, particularly fueled by the rise of institutional and retail lenders. These firms aggregate capital by guaranteeing an interest rate to depositors and then lend those funds out to institutional investors or retail individuals. The largest firms include Genesis Capital, BlockFi, and Babel Finance. The primary difference between these lenders is what type of investor makes up their deposit base — institutional or retail.

This type of lending activity really took off in 2018 as institutional investors looked for more efficient ways of short selling cryptocurrencies. In the latter two quarters of 2018 alone, Genesis Capital was able to originate over $1b in crypto loans from institutional investors. 2019 brought with it a bull market which spawned the advent of cash lending. These lenders saw explosive demand for crypto backed cash loans and the ability to offer retail investors yield on their dollars. Based on the figures included in Genesis’s Q4 2019 report as well various industry reports, we estimate that over $5 billion USD has been originated by institutional and retail lenders, 40% of which is cash loans.

These centralized lenders are extremely liquid given they were designed to serve institutional capital. Most lending agreements are open term, meaning the borrower and lender have some flexibility on capital lock ups. Returns are generally higher than lending through an exchange and custom terms can be negotiated for large dollar sizes. The main downside is counterparty risk and custody of funds. In these agreements, the lending firm takes full custody of lent funds and then transfers ownership to the borrower. In the case of a default, the lender is trusting the lending firm to cover losses.

Lending Protocols

Lending protocols are a completely net new financial innovation uniquely enabled by crypto rails. These platforms allow users to borrow and lend money directly from a smart contract, without having to give up custody of their funds to a centralized third party, a stark contrast to today’s most dominant centralized models. The key to these protocols is that they’re built on top of virtual machines that autonomously handle all parts of the loan administration process, from origination to liquidation, a centralized entity doesn’t need to be involved.

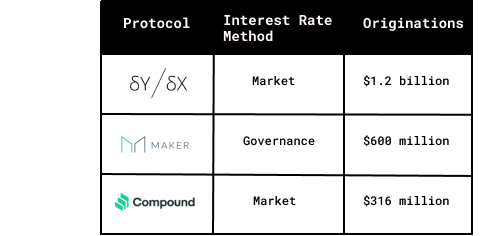

The most widely used lending protocols are MakerDAO, Compound, and dYdX. Maker is unique in that interest rates are ultimately set by MKR holders via the network’s governance process, whereas rates in Compound and dYdX are set in real time by the market. Similarly, Maker’s Dai savings rate can never be higher than the stability fee, whereas Compound and dYdX often offer rates higher than the stability fee because the protocols can more quickly adjust to speculative demand.

DeFi lending protocols are still relatively new so it’s naturally going to take some time until they’re as liquid as their centralized counterparts. Two big factors that will help these protocols increase liquidity are security best practices and time. The former will help expose and innovate on weaknesses inherent to these protocols and the latter will help reinforce the safety of these protocols assuming they remain secure. An area where lending protocols excel is custody since users are always in control of their funds, there is less risk of a theft relative to a centralized exchange. Returns vary based on where the capital is being lent. Lending on more speculative venues that enable more leverage, like dYdX, offer higher returns because more notional value can be borrowed.

Automated Market Maker Models

Automated market maker (AMM) systems enable anyone to play the role of market maker by allowing them to pool two sided liquidity that traders can tap into. In exchange for their liquidity, suppliers earn a yield. Within crypto specifically, AMMs have been used as a solution to the liquidity issues faced by decentralized exchanges that employ basic maker-taker systems. AMMs make it much easier to bootstrap markets since anyone in the world can act like a market maker.

Two notable AMM projects opening up dollar yields to investors are Uniswap and Balancer. Uniswap was the first AMM system to gain real traction, which it did by opening up liquidity for DeFi assets that were not widely supported on centralized exchanges like MKR and SNX. Balancer extended the Uniswap concept further by enabling pools with more than two assets. In both of these models, liquidity providers earn yield by collecting trading fees generated by each pool.

Like DeFi lending protocols, AMMs are still extremely new so liquidity isn’t strong. For context, the ETH<> DAI and ETH<>USDC Uniswap pools only have $6.7 million and $4.9 million in liquidity respectively. Counterparty risk is low from a self custody perspective, but high from an experimental technology perspective. Returns offered by AMM models are different from basic asset lending. Many times, supplying liquidity to these pools in search of a yield is akin to a short volatility position, so investors can actually lose money during times of turbulence. There are also instances in which growth in the size of the pool mitigates the effect volatility has on potential returns. Overall, returns provided by AMM models are higher, but riskier. For a deeper overview of the return profile, check out Pintail’s work here.

Derivatives

When most people think of cryptocurrency derivatives, they think of purely speculative use cases, when in fact, cryptocurrency derivatives offer clever solutions for earning dollar yields. An important aspect of these derivatives is the fact that they’re margined and settled in the base currency, so in the case of crypto BTC and ETH, but quoted against USD. This means that short positions effectively lock in the dollar value of the notional position because even if the price increases, the value of the collateral backing the position also goes up.

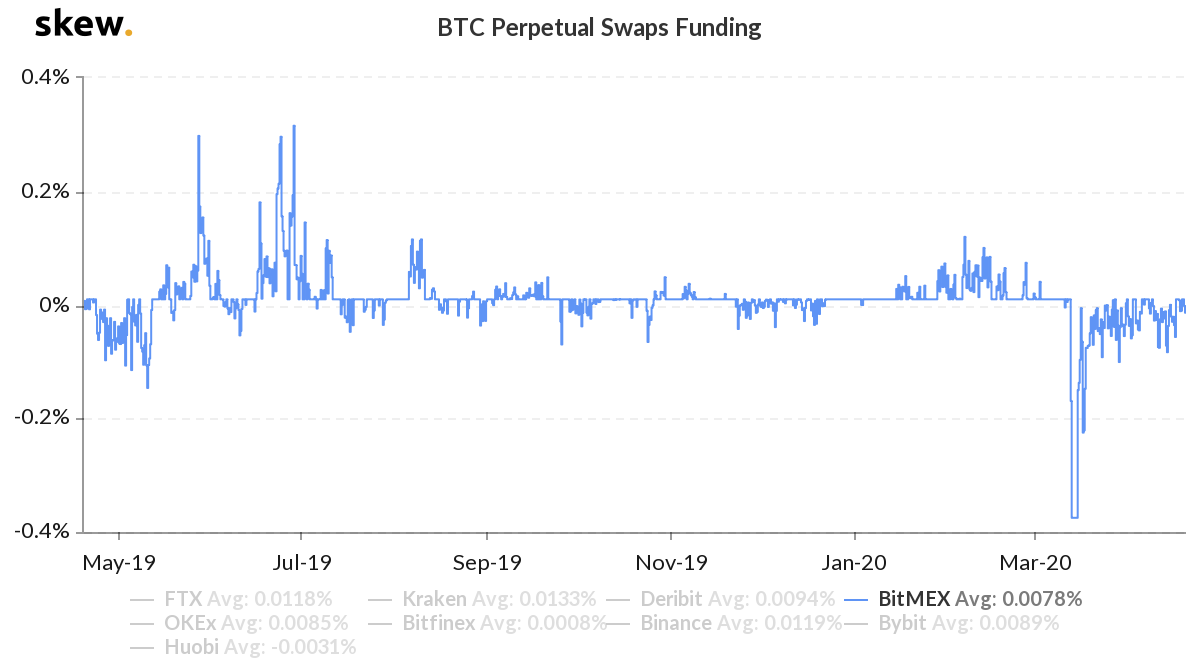

Not only do these short positions act as synthetic dollars, they can also earn a yield if the market pays a premium to hold these derivative contracts. If users are short through a perpetual swap, they are paid interest every funding window. If they are short through a traditional futures contract, they collect the annualized forward premium over the duration they have the position open. Interest earned is very much correlated with how bullish the market is. In 2017, there were many times in which BitMex’s XBTUSD contract was paying out over 1% in interest per day. More recently, this number has come down, likely in part because of more traders entering synthetic USD positions. In the last year, XBTUSD has paid out over 8% in synthetic dollar interest.

Synthetic dollars are created through futures contracts, with perpetual swaps being the most liquid way of doing so. Futures are by far the most liquid way to get exposure to crypto, they facilitate billions in trading volume daily. Compared to other lending options, synthetic dollars are very liquid. However, a big downside is that synthetic dollars can’t leave the exchange, the positions have to be held until expiry. This means that users still bear a lot of counterparty risk, centralized exchanges are much more susceptible to hacks and thefts. Luckily for synthetic dollar holders, the added risk does come with a higher reward — during times of high contango, yields often spike above 20% apr.

Conclusion

One of the most powerful use cases enabled by cryptocurrencies today is the ability to earn dollar denominated yield. Already, the crypto financial services ecosystem has birthed a variety of dollar yield sources including centralized exchanges, institutional and retail lenders, decentralized lending protocols, automated market makers, and synthetic dollars through derivative exchanges. With all of these options, users have optionality across a number of features like liquidity, custody, risk, and potential returns.

As you can see, there are clear trade-offs for investors chasing the highest potential returns. Lower liquidity is the main trade-off for decentralized finance platforms and counterparty risk is the main trade-off for derivatives.

Crypto dollar yields will continue to pull people away from the traditional world. As these offerings mature, so will the ability to onboard more capital into the crypto world. At dYdX we are excited about the future of crypto dollar yields and the role we play in providing non-custodial, liquid on ramps to dollar yields. Similarly, we pride ourselves on being the only venue that allows users to both lend their crypto dollars to a decentralized lending protocol as well as access synthetic dollars through our perpetual markets.

Get early access the BTC Perpetual Market or start using dYdX today.

You can reach dYdX via email at contact@dydx.exchange, on twitter, or on our official telegram.